The Indonesian chemical industry started to grow again in 2009 after the global economic crisis in the last quarter of 2008. The improving trend continued through 2010 as reflected by the increase in the consumption of plastic basic material from the upstream petrochemical industries. With a huge domestic market, low plastic consumption per capita, and high industry growth, the chemical industry offers promise but also faces several problems such as low utilization of production capacity, high prices for basic materials and high import prices. In addition, a lack of integration between the petroleum and petrochemical industries has become an obstacle to the industry’s development.

The implementation of the ASEAN-China Free Trade Area has led the flood of imports of chemical products to Indonesia. This can be seen from the increased number of imports of some chemical products upstream and midstream. Meanwhile, exports of chemical products have not shown significant improvement due to the problem of gas supplies and surging oil prices.

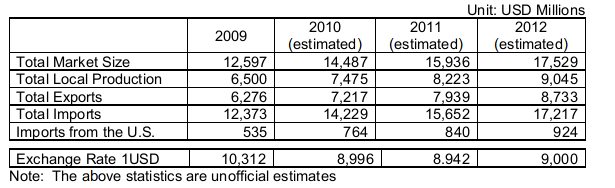

Indonesia imported $12.3 billion worth of industrial chemicals in 2009. In 2010, the total import value of chemical products is estimated to reach $14 billion. Imports of U.S. products represented only 5.4 percent of the total import value. The actual import value of U.S. products could be higher than reported, because many U.S. products are imported to Indonesia through Singapore.

In 2010, U.S. imports are estimated at $764.1 million, broken down as follows: $90 million inorganic chemicals (HS 28); $241 million organic chemicals (HS 29); $38.2 million chemical pharmaceuticals (HS 30); $14.2 million other chemical fertilizers (HS31); $20.5 million chemical dyes (HS 32); $37.2 million essential oils & perfumes (HS33); $119.3 million other chemicals (HS 38); and $202.9 million plastic products and raw materials (HS 39).

U.S. suppliers face strong competition from other countries such as Singapore, Japan, China, South Korea, Thailand, Germany and the United Kingdom. International companies such as Dow Chemical, Union Carbide, BASF, DuPont, LG, Hoechst, and Ciba Chemicals are among the significant industrial chemical players with manufacturing operations in Indonesia. In general U.S. products are well accepted, but they are perceived as high-priced products.

U.S. companies are strong suppliers of carbonates, epoxides, medicaments, ink, odoriferous mixture, make up, reaction initiators, insecticides, polyamides, polymers of ethylene, and polyethers.

Currently, more than 50 percent of the raw material demand from various industries such as plastic, textile, pharmaceutical, electronics, automotive components, ceramics and glass is supplied by imported products. Besides facing the shortage of raw materials, the chemical industry in Indonesia faces a lack of infrastructure facilities, inefficient and small-scale operations, and limited financial resources.

Indonesia’s petrochemical industry is still heavily dependent on imports for feedstock including naphtha for olefin and condensate for aromatic. Indonesia is also still dependent on imports of inorganic chemicals. Some of inorganic chemical products have not yet been produced in Indonesia, such as aluminum, sodium cyanide and soda ash. Indonesia is one of the largest importers of pharmaceutical raw materials in the world indicating that Indonesia is a huge market for pharmaceutical chemical products.

U.S. suppliers in this industry will have opportunities to supply raw material for those various industries and to introduce new technology to develop plants in Indonesia.