Value-Added Tax

A person or body, in whatever form, which in the course of its operations, produces, imports or exports taxable goods, conducts trading activities or renders taxable services, is required to register as a Taxable Entrepreneur with the DGT. However, only a resident or a PE can obtain a VAT registration. Registration by non-residents is not allowed

The rate of VAT is 10 percent but under the law the government may amend this rate to a minimum of five percent and a maximum of 15 percent. VAT is levied on exports at zero percent.

Goods and Services Subject to VAT

VAT is imposed on:

- The delivery of taxable goods (tangible or intangible) in the Indonesian customs area by an entrepreneur

- The importation of taxable goods

- The rendering of taxable services in the Indonesian customs area

- Utilization in the customs area of intangible taxable goods from outside the Indonesian customs area

- Utilization of offshore taxable services in the Indonesian customs area

- Export of taxable goods by an entrepreneur

- The activities of self construction

- The disposal of fixed assets by a Taxable Entrepreneur including the transfer in the course of a merger (except where VAT on the original acquisition could not be credited).

Special schemes for VAT apply to sales of cigarettes, pre-recorded cassette tapes and compact discs.

Collection, Filing and Payment of Tax

VAT is determined by applying the tax rate of 10 percent to the sale, replacement or import price. The sales price is the money value including all costs of delivery, installation, insurance, technical and maintenance, commission, guarantees, interest and others, as long as they relate to the delivery of goods. Compensation for services is the money value, including all costs, which relate to the delivery of the services.

Excluded from the sales price, are sales tax and discounts and rebates, as long as these are included on the tax invoice.

For imported goods, the import value is the value used as the basis for calculating the import duty together with other levies imposed on the basis of the provisions in the customs law, but excluding VAT and STLG.

In cases where a special relationship exists between two parties involved in a transaction, the DGT may substitute a market price that becomes the basis on which the VAT is charged.

Monthly remittances are required for the excess of output VAT over input VAT. Output VAT is VAT charged by a taxable entity on its sales of goods and services. Conversely, input VAT is the VAT incurred on purchases of goods and services used in the business. If input VAT exceeds output VAT for any month, a refund can be claimed. A refund claim triggers a tax audit. Input VAT, supported by a valid tax invoice, is only creditable if it is reported within three months after the end of the period stated in the tax invoice.

There is a self-collection obligation in relation to input tax on offshore services purchased from non-residents for the benefit of residents.

Certain government bodies, production sharing contractors and mining companies are subject to special rules as they are designated VAT collectors. These bodies are obliged to remit VAT related to their purchases directly to the tax authorities.

Credit of Input VAT

Input VAT can be credited against output VAT except for:

- Purchases not directly for business activities (e.g. costs for staff welfare or benefits)

- Purchases before registration as a “VAT-able” business

- Purchases of certain passenger vehicles

- Purchases with an incomplete VAT invoice

- VAT stated in a simple VAT invoice

- VAT collected through an assessment notice

- VAT not declared in the VAT return which is discovered in a tax audit

- VAT on expenditure relating to activities which are not subject to VAT.

Exemptions and Reliefs

The principal activities not subject to VAT are as follows:

- Goods produced by mining or drilling that are taken directly from their source, i.e. crude oil, natural gas, geothermal energy, sand and gravel, coal (before processed into briquettes), and ores of iron, tin, gold, copper, nickel, silver and bauxite

- Basic necessities needed by the populace as a whole, i.e. rice, corn, sago, soybeans and salt

- Money, gold ingots and negotiable instruments

- Banking, insurance, leasing services and securities

- Manpower services

- Social, health, religious and education services

- Public transportation, postal services, non-commercial broadcasting

- Entertainment services

- Hotel and catering services

- Government services.

The following goods and services are granted an exemption from VAT:

- Machinery and capital equipment in certain situations

- Electricity (unless for housing with capacity exceeding 6600 watts)

- Piped water

- Livestock, poultry and fish feed and/or raw materials for the preparation thereof ●Certain agricultural crops in their natural state delivered by farmers

- Seeds from agricultural, plantation, forestry, animal husbandry, breeding and fishery sources

- Polio vaccines

- Textbooks

- Charter or purchase of ships used by national shipping and fishing companies, together with related components

- Charter or purchase of aircrafts used by national airline companies, together with related components

- Purchase of railway trains by PT Kereta Api Indonesia and related components

- Construction and sale of simple houses of various types

- Equipment and supplies of certain kinds used by Defense and Police forces.

Relief for Export Manufacturers

There are a number of relief schemes to allow exporter manufacturers to operate on a virtually VAT and duty-free basis. Such schemes include bonded zones, economic development zones (KAPET) and free trade areas. The Government has approved a number of Bonded Areas located throughout Indonesia.

Free trade areas and free ports are located in Indonesia but are considered outside the customs area and, therefore, goods brought into these areas are exempt from import duties, VAT and STLG. Business activities that can be carried out in a free trade area include, among others, trade, services, mining, transportation, banking and manufacturing. Sabang, Batam, Bintan and Karimun are currently the free trade areas in operation.

An import incentive is granted to a manufacturer who imports raw materials to be used for processing, assembling, or installing in goods, provided those goods will be 100 percent exported. A manufacturer must be registered in order to be entitled to this incentive. A bank guarantee or customs bond is required for the full amount of the import duty, excise, VAT and STLG that would otherwise have been payable. When the goods are exported, the guaranty or bond is released. A refund can be granted on any import duty, excise and tax paid on imported goods that are later used in producing items for export. Under this facility, 25 percent of the goods may be sold on the domestic market provided the duties and taxes are paid on that portion.

Sales Tax on Luxury Goods

The VAT law also imposes a STLG on deliveries of luxury goods by manufacturers in Indonesia and on the importation of luxury goods. The rates vary depending on the category of the goods. The current rates range from 10 percent up to 75 percent, although the Law allows for a maximum of 200 percent. Conceptually, this tax is charged only once. Like VAT, STLG is charged at zero percent on the export of luxury goods and any STLG suffered may be reclaimed. STLG is calculated by multiplying the applicable rate against the sales price or import price, excluding VAT. The STLG payable on the purchase of luxury goods cannot be credited against the VAT collectable when the goods are subsequently sold.

In broad terms, some of the main types of goods subject to STLG include:

- Passenger vehicles

- Alcoholic beverages

- Certain food and non-alcoholic beverage products

- Household appliances and electronic goods

- Cosmetics

- Luxury homes and apartments.

It is necessary to determine the applicability of the STLG on a case-by-case basis as the rules are complex and subject to change. There is an exemption from STLG on certain items for public use.

Customs Duties

Customs duties are imposed on items imported into Indonesia. Customs duties are generally imposed on an ad valorem basis.

Duties are payable based on the Harmonized System (HS) classification. Duties are based on the cost, insurance and freight (CIF) value of the imported item and, in general, are imposed at rates of zero percent to 20 percent for most goods, 25 percent to 80 percent for cars, and 170 percent for alcoholic drinks.

Since April 1997, new Customs procedures have been in force. These procedures are based upon General Agreement on Tariffs and Trade (GATT) principles. The previous system of pre-shipment inspection by independent surveyors was replaced with post-arrival control procedures exercised by Department of Customs officials.

Some key features of the current system are:

- Ports have a red and green channel system for imported goods. Red channel goods are all inspected. Green channel goods should not normally be inspected unless there is some justification

- Duties and taxes shown on the import declaration must be paid through a designated bank in order for the goods to be released

- Valuation of goods is based on GATT conventions

- The accuracy of the declaration and value is subject to subsequent audit of the importer’s records.

Simplified procedures apply for goods entering bonded areas. Special rules apply for imports in the oil and gas sector, and goods for government projects funded by loans or grants from other governments.

Import duties are not payable in certain circumstances including:

- Imports used in the production of exports where the manufacturer is located in a bonded zone or free trade area or which are registered for the KITE (import facility for export purposes) facility, formerly known as the Bapeksta facility

- Certain imports by the petroleum, geothermal and mining industries.

Other relief includes:

- For certain goods, which are imported on a temporary basis, the importer must pay 2 percent of the import duty and VAT each month for the period of usage. The remaining amount can be guaranteed. If the goods are not re-exported, the full amount of import duty and taxes plus a 100 percent penalty on the import duty must be paid

- Import duty tariffs are reduced to five percent on importation of goods by approved foreign and domestic investment companies using Master list facilities.

The ASEAN Free Trade Area (AFTA) is a free trade area covering the members of Association of South East Asian Nations (ASEAN). Under AFTA, ASEAN will become a free trade area with no tariff or non-tariff barriers on cross border transactions between ASEAN countries by 2015. To achieve the AFTA goal, the Common Effective Preferential Tariff (CEPT) was introduced as a mechanism to lower tariff rates on a wide variety of goods.

The first six signatories to the CEPT scheme – Brunei Darussalam, Indonesia, Malaysia, the Philippines, Singapore and Thailand – agreed to reduce tariffs to zero percent to five percent on a large number of goods. These countries also agreed to the elimination of import duties on all Inclusion List goods traded in AFTA by 2010. The other four ASEAN member countries – Cambodia, Laos, Myanmar and Vietnam – have agreed to eliminate tariff barriers by the year 2015.

Excise Duties

Excise duties are levied on specific products whose consumption is restricted or controlled, namely alcoholic beverages and tobacco products.

Stamp Duty

A stamp duty tax of either Rp 3,000 or Rp 6,000 is charged on certain documents such as receipts, agreements, powers of attorney and other legal documents.

Tax on Land and Buildings

This is a tax levied on the holding of land or buildings within Indonesia. The DGT, or in practice delegated regional authorities, will initially determine who the taxpayer is and issue a Report On The Tax Object to that property. Normally, the owner is responsible for paying the tax due.

Tax Rate and Method of Calculation

Tax is currently imposed at 20 percent or 40 percent of the full statutory rate, which is 0.5 percent of the sales value of the tax object. Thus, the actual tax rate is 0.1 percent or 0.2 percent. The sales value is the actual transaction price or, in the absence of a transaction, the price of a similar object can be used. The law provides that the sales value is to be fixed every three years, except for certain areas where it is fixed annually.

The tax is to be determined for the tax year, being the calendar year, based on the condition of the land and buildings as at January 1. Specific calculation formulae are stipulated for plantations, mining and forestry businesses.

Collection of Tax

The MOF has delegated authority to collect the tax to the governor/chief of the special region of Jakarta and regents/majors/heads of second level regions, except for tax on land and buildings involving taxpayers with plantations, forests, and mines.

The law provides that the relevant authority is to forward to the taxpayer a Report On The Tax Object, which is to be completed and returned within thirty days of receipt. Based on this report, a Notification of Tax Due will be sent to the taxpayer indicating the amount of tax which is then payable within six months.

Exemptions

The law exempts buildings with a fair market value of less than Rp 12,000,000 and land and buildings that are used:

- For not-for-profit activities for the purpose of religious worship, social affairs, health, national education and culture

- For graveyards and archaeological relics

- As protected forests, nature reserves, tourist forests, national parks, pasture under village control and other state lands

- For diplomatic offices or consulates on a reciprocal basis

- By specified international organizations.

A 50 percent reduction is allowed for hospitals, nursing homes, orphanages and nonprofit schools, among others.

Property Title Transfer Tax

A transfer tax is payable on every transfer of title of land, or land and buildings. The taxpayer is the recipient of the rights.

The definition of “transfer” is broadly defined, and includes:

- A sale and purchase transaction

- An exchange of assets

- A grant or a gift

- A testamentary grant

- The enforcement of a judicial ruling with permanent legal force

- A business merger, liquidation or expansion.

Exemptions

Tax is not imposed on certain transfers, such as:

- Transfers of title to the state for the public interest

- Transfers to diplomatic representatives and certain international organizations

- Donations for certain religious and community purposes.

Tax Rate and Method of Calculation

The tax is five percent of the transfer price. There is a non-taxable amount of Rp 60 million. The amount to be taxed is the acquisition cost. If the deemed sale value determined for land and buildings tax purposes is higher, that amount will be used as the basis for the transfer tax.

The property title transfer tax can be reduced in certain cases, including:

- Grant of property to certain close family members – 50 percent reduction

- Transfer of property in an approved merger or consolidation – 50 percent reduction

Collection of Tax

This tax becomes payable before the transfer is legalized. The lawyer or notary cannot legalize any legal documents in relation to the transfer if the tax has not been paid. The tax authorities are granted the power to review the property title transfer tax. If any underpayment is found, the tax authorities can issue a tax assessment.

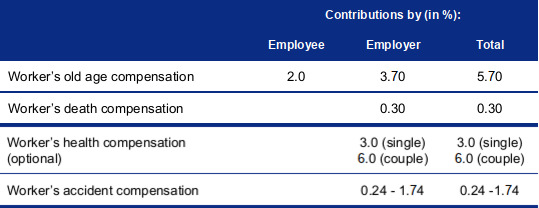

Payroll Taxes

There are no additional payroll taxes in Indonesia other than the employee income tax withholding system. However, the social security contributions (JAMSOSTEK) are based on payroll, most of which are borne by the employer.

Workers’ health compensation is payable only where the employer does not provide equivalent or better health provisions. Under the current regulation, an expatriate is required to join JAMSOSTEK unless covered by an equivalent program in his or her home country.

Death, Gift and Inheritance Taxes

No gift and inheritance tax is levied in Indonesia.

Fiscal Tax

Effective January 1, 2009, a fiscal tax of Rp 2,500,000 was payable upon departure from Indonesia by residents who did not have a tax identification number (NPWP). This fiscal tax was abolished from January 1, 2011.

Regional and Local Taxes

The local governments collect regional and local taxes. These taxes include:

- Entertainment tax

- Advertisement tax

- Motor vehicle taxes

- Hotel and restaurant tax

- Street lighting tax

- Tax on the use of underground and surface water.