Overview

The principal taxes applicable to companies doing business in Indonesia are the corporate income tax, branch profits tax, resource royalty tax, withholding tax, value added tax (VAT) and various other indirect levies, such as tax on land and stamp duty. There is no excess profits tax or alternative minimum tax.

Residence

A company is considered resident in Indonesia if it is established or domiciled in Indonesia.

Taxable income and rates

Resident companies are taxed on worldwide income. Nonresident companies are taxed only on Indonesia-source income, including income attributable to a permanent establishment (PE) in Indonesia.

Companies pay tax on taxable pofits at a flat rate of 25%. Resident corporate taxpayers with gross revenue up to IDR 50 billion receive a 50% reduction in the corporate tax rate imposed on the taxable income for their gross revenue up to IDR 4.8 billion. PEs are subject to a branch profits tax of 20% (or a lower rate under a tax treaty) on net after-tax profits, in addition to the corporate income tax rate. A public company that has at least 40% of its total paid-up shares traded on a stock exchange in Indonesia and that complies with other requirements can obtain a 5% reduction in the income tax rate.

Taxpayers engaged in certain business sectors, such as construction and shipping, pay income tax at certain percentage of gross income.

Taxable income defined

Taxable net income is defined as assessable income minus tax-deductible expenses. Exempt income includes contributions to capital, dividends from domestic companies, and certain income from investment funds and venture capital companies.

Deductions

Most expenses incurred in deriving business income may be deducted, including wages, fees, interest, rent, royalties, travel expenses, bad debts (subject to certain qualifications), insurance premiums, administration costs and levies, depreciation and amortization, operating losses and contributions to approved pension funds.

Nondeductible items include the payment of dividends, unapproved reserves, fringe benefits, charitable contributions and the income tax itself.

Depreciation

Assets with a beneficial life of more than one year may be depreciated using the straight-line or declining balance method, as follows:

Category 1: 50% (declining balance) or 25% (straight-line) on assets with a useful life of four years (furniture/equipment constructed of wood/rattan, office equipment, computers, printers, scanners, special tools for related industries/services, motor vehicles for transport, warehousing and communications).

Category 2: 25% (declining balance) or 12.5% (straight-line) on assets with a useful life of eight years (furniture and equipment constructed of metal, air conditioners, cars, buses, lorries, containers, light industrial machinery, logging equipment, construction equipment, heavy vehicles for transport, warehousing and telecommunications equipment).

Category 3: 12.5% (declining balance) or 6.25% (straight-line) on assets with a useful life of 16 years (machinery for general mining other than oil and gas; machinery for textiles, chemicals and

machine-building industries; heavy equipment, docks and vessels for transport and communications; and assets not included in other categories).

Category 4: 10% (declining balance) or 5% (straight-line) on assets with a useful life of 20 years (including heavy machinery for construction, locomotives, railway coaches, heavy vessels and docks).

Building category: 5% (straight-line) on permanent buildings with a useful life of 20 years, or 10% (straight-line) on non-permanent buildings with a useful life of 10 years.

Decrees issued by the Ministry of Finance specify which assets are included in each category. Separate lists of assets and depreciation rates apply for the oil and gas sector and special options apply to investment in remote locations. Investors need approval from the DGT to change from the straight-line to the declining balance method, and vice versa. Assets may be revalued. Revalued assets begin depreciating from their new value.

Establishment and expansion expenditure can either be expensed or amortized at the rates prescribed by law (that is, four classes of intangible assets with useful lives of four, eight, 16 or 20 years, and different depreciation rates depending on the method—straight-line or declining balance). Tax incentives providing for accelerated depreciation are available for businesses that locate in certain regions.

Losses

Losses may be carried forward for five years following the year the loss was incurred and 10 years for certain industries that benefit from tax incentives. The carryback of losses is not permitted.

Capital gains taxation

Capital gains are taxable as ordinary income, and capital losses are deductible. However, the sale of shares listed on the Indonesian stock exchange are subject to a tax of 0.1% of the transaction value. Founder shares also are subject to an additional final tax of 0.5% on the share value at the time of an initial public offering, regardless of whether the shares are held or sold following the offering.

The sale or transfer of land and/ or buildings is subject to a 5% income tax on the sales proceeds.

Capital gains derived from the sale of Indonesian assets held by foreigners are taxable at a rate of 5% of the gross proceeds, unless the rate is reduced under a tax treaty.

Double taxation relief

Unilateral relief

Resident companies deriving income from foreign sources are entitled to a unilateral tax credit for foreign tax paid on the income. The credit is limited to the amount of Indonesian tax otherwise payable on the relevant foreign income. A country-by-country limitation applies, i.e. the credit for foreign tax paid on income from one country is limited to the amount of Indonesian tax otherwise payable on the income from the same country. Indonesia does not grant credit for underlying tax.

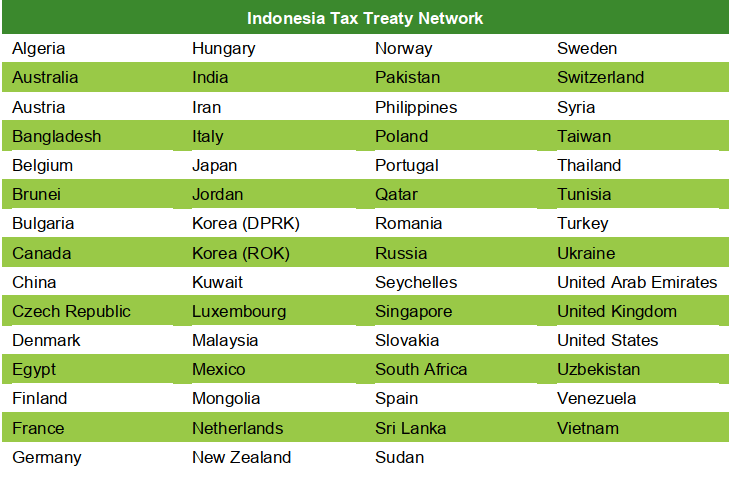

Tax treaties

Indonesia has a reasonably broad tax treaty network. To claim relief under a tax treaty, the foreign taxpayer must complete and submit to the Indonesian tax authorities a specific document issued by the Indonesian Tax Office in lieu of a company that is a banking institution or earns income from bonds or stocks listed on the Certificate of Domicile, and Form DGT-1 or Form DGT-2. Form DGT-2 is specifically for a Indonesian stock exchange. The Certificate of Domicile must be endorsed by the tax authorities of the tax treaty partner country. If the foreign taxpayer is unable to obtain the endorsement, the foreign taxpayer can use any form of Certificate of Domicile commonly verified or issued by the tax treaty partner’s tax authorities, provided certain requirements are met. This form must be attached to a completed Form DGT-1 or Form DGT-2. Treaty relief will be denied if the foreign taxpayer fails to fulfill this requirement.

Anti-avoidance rules

Transfer pricing

The DGT requires that related party transactions or dealings with affiliated companies (including profit sharing by multinational companies) be carried out in a “commercially justifiable way” and on an arm’s length basis. Taxpayers are required to maintain supporting documentation on related party transactions, which at a minimum should cover the taxpayer’s transfer pricing policy, price or profit (including transfer pricing methodology). A detailed transfer pricing guideline has comparability analysis, selected comparables and explanation on determination of arm’s length been issued along the lines of the OECD approach to transfer pricing issues.

Thin capitalization

Indonesia does not have specific thin capitalization rules, although the income tax law authorizes the Ministry of Finance to determine the debt-to-equity ratio of companies for tax calculation purposes.

Controlled foreign companies

A CFC is a foreign company in which an Indonesian resident company or an individual holds at least 50% of the registered capital (either alone or together with other resident taxpayers). The CFC rules apply only to unlisted foreign companies. Indonesia does not have a white or black list of countries.

If the CFC rules apply, the Minister of Finance is authorized to determine when a dividend is deemed to be derived by the Indonesian resident shareholder if no dividends are declared. Dividends are deemed to be derived from a foreign company where an Indonesian resident taxpayer holds at least 50% of the paid-up capital of the foreign subsidiary or, together with other resident taxpayers, holds at least 50% of the paid-up capital. This applies only if the foreign company does not trade its shares on the stock exchange. If no dividends are declared or derived from the offshore company, the resident taxpayer must calculate and report the deemed dividend in its tax return; otherwise, the Ministry of Finance will do so. The dividend is deemed to be derived either in the fourth month following the deadline for filing the tax return in the offshore country or seven months after the offshore company’s tax year ends if the country does not have a specific tax filing deadline.