The CoW company is the sole contractor for all mining in the CoW area other than for oil and gas, coal and uranium. The company has control, management and responsibility for all its activities, which include all aspects of mining from exploration, development, production, refining, processing, storage, transport and sale.

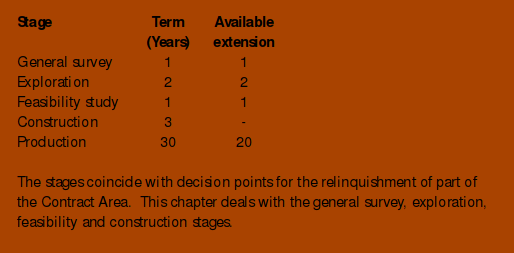

The CoW outlines a series of stages with defined terms:

CoW OBLIGATIONS

On signing the CoW, the company is required to lodge a US dollar security deposit with the Department of Mines and Energy, which is released on completion of the following:

- Satisfactory completion of the General Survey period (25%);

- At the end of the first year of the Exploration stage and after the company has submitted satisfactory quarterly reports (25%);

- On submission of a general geological map to the Department within 12 months of completion of the Exploration Stage (25%); and

- On submission of the completed Feasibility Study to the Department (25%).

During the preproduction stage the company is required to submit detailed quarterly progress reports to the Department. Under the CoW, the company has responsibility for all financing requirements of the project and details are to be reported to the Department of Mines and Energy.

The CoW imposes obligations on the company throughout the life of the CoW with respect to environmental restoration, the employment and training of Indonesian nationals, preference to Indonesian suppliers, and the provision of infrastructure for the use of the local population. In addition, the company has the following obligations under the CoW.

GENERAL SURVEY STAGE

In the General Survey stage, the company is obliged to spend an agreed amount during the 12-month period. At the end of the period, the company has to submit a report detailing the items and amount of expenditure. At the end of this period the company is required to relinquish at least 25% of the original Contract Area.

EXPLORATION STAGE

In the Exploration stage, the company is obliged to spend an agreed amount per year on exploration activities. At the commencement of this stage, the company must submit an annual program and budget to the Department.

At the end of the Exploration stage, the company is required to file with the Department:

- A summary of its geological and metallurgical investigations and all data obtained; and

- A general geological map of the Contract Area.

On or before the second anniversary of the Exploration stage the company is required to have reduced the Contract Area to not more the 50% of the original Contract Area.

FEASIBILITY STUDY STAGE

At the end of the Feasibility Study stage the company is required to submit a feasibility study, including environmental impact studies, to the Department and to design the facilities.

At the end of the Feasibility Study, the company is required to have reduced the Contract Area to not more than 25% of the original Contract Area. The Contract Area at this point cannot be greater than 62,500 hectares.

CONSTRUCTION STAGE

The company undertakes the construction of the facilities.

DEAD RENT

Throughout the life of the CoW, the company is required to pay dead rent. This is an annual amount based on the number of hectares in the CoW area and the stage of the CoW. For example, during the first year of the Exploration stage, the dead rent is US$0.10 per hectare.

TAX TREATMENT OF EXPENDITURE

Note that the tax treatments described in this booklet relate specifically to the 7th generation CoW. Appendix 1 sets out the differences between the various generations of CoWs. Appendix 2 demonstrates the operation of a number of the tax provisions described below.

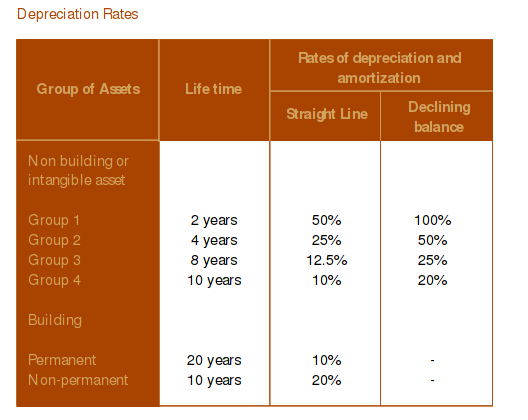

FIXED ASSETS

Fixed assets in the Contract Area may be depreciated under either the diminishing value or straight-line method. The rates of depreciation are specified in the CoW and are generally accelerated, with most equipment being depreciated over an 8-year effective life (25% diminishing value; 12.5% straight-line). A full year’s depreciation is allowed in the first year of use. Table 1 sets out the rates of depreciation.

Infrastructure assets such as buildings, roads, bridges, educational and medical facilities are also depreciable. Assets are required to be accounted for on an individual basis rather than a pool of undepreciated cost.

Group 1 assets include furniture and equipment constructed of wood/rattan; motorcycles; office equipment, special tools for specific industries/services, kitchen equipment and light machinery for the food and drink industry.

Group 2 assets include furniture and equipment constructed of metal, air conditioners, computers, printers, scanners, cars, buses, trucks, containers and the like; equipment for construction, heavy vehicles for transportation, warehousing, and communication and telecommunication equipment.

Group 3 assets include machinery for general mining other than oil and gas, heavy equipment, docks and vessels for transportation and communication and other assets not included in the other categories.

Group 4 assets include heavy machinery for construction, locomotives, railway coaches, heavy vessels and docks.

PRE-PRODUCTION EXPENSES

Expenses incurred prior to production with a useful life greater than one year should be capitalized for amortization under either the diminishing value or straight-line method once production has commenced. These expenses can also include expenditures incurred by the CoW company’s shareholders prior to the formation of the CoW company, provided the expenditure has been audited.

Where the useful life of the expenditure is less than one year, the expenses are required to be expensed in the year they are incurred. This will give rise to a tax loss, which can be carried forward. In practice, many companies treat all expenditure as having a useful life greater than one year.

Care needs to be taken with the transfer of pre-production costs accumulated in either the offshore investor’s accounts or a service company, as there may be VAT and withholding tax implications.

INTEREST EXPENSE

Interest expense paid on loan capital is deductible as long as the debt to equity ratio does not exceed:

- 5:1 for investments up to US$200 million

- 8:1 for investments greater than US$200 million

and the interest does not exceed commercially available rates. Where interest is paid to an offshore lender, withholding tax will be payable subject to the relevant tax treaty. Where funds are provided interest free, unless agreement has been sought from the tax authorities, it is likely that interest will be deemed on the funding.

LOSS CARRY FORWARD

Under the CoW, tax losses can be carried forward for up to eight years and are recouped on a first-in, first-out basis. Tax losses cannot be carried back.

VAT

CoW companies are designated as VAT Collectors by the State Treasury. This means that they pay VAT directly to the Treasury, rather than to their suppliers.

During the pre-production stage of the CoW, the company will have no output VAT and will collect and pay all its input VAT to the Government. The company can claim back input VAT on an annual basis. In order to receive a refund the company must undergo a thorough tax audit.

All VAT payments are denominated in rupiah. Where a company keeps its books in US dollars, this can give rise to an exchange risk and should be carefully managed.

IMPORTATION OF CAPITAL EQUIPMENT

The 7th generation CoW provides exemptions from import duties, VAT and income tax on the importation of capital equipment in accordance with the prevailing law. Exemptions may be available under the general law and careful planning is recommended to take advantage of any such exemptions.

Where a company has imported capital equipment free of VAT and import duties, if the company does not subsequently re-export the equipment, it may be subject to VAT and import duties at a later time.