Registration

All taxpayers are required to register for income tax purposes. A non-resident foreign company is only obliged to register if it has a PE as defined in the domestic tax law or applicable DTA. Upon registration, a taxpayer identification number (NPWP) is obtained. The DGT may register any person who, in its opinion, should be registered as a taxpayer. Subsequently, that person must meet all obligations stated in the law. According to the new General Tax Provisions and Procedures Law, if an NPWP is officially issued by the DGT, as opposed to voluntary registration, an assessment may be issued in relation to tax years up to five years prior to the issuance of the NPWP.

A taxpayer must deregister with the DGT when it ceases to be a taxpayer in Indonesia. The DGT will generally perform a tax audit in order to ensure that the taxpayer has met all obligations. Until the DGT deregisters the company, all obligations stated in the tax law continue to apply. Under the new Law, there is now the following time limitations for the DGT to complete the de-registration application:

● 6 months for individual taxpayers

● 12 months for corporate taxpayers

● 6 months for taxable entrepreneur (PKP – VAT registration).

Tax Installments

Corporate and individual taxpayers must pay monthly income tax installments. For most taxpayers, installments are based on the income tax payable, as reflected in the annual corporate income tax return of the prior year, after deducting taxes withheld and collected by other parties in that prior year divided by 12. For the months of a fiscal year prior to lodgement of the prior year return the installments will be equal to the December installment of the prior year (or the last month installment of the prior year for a corporate with a non calendar fiscal year). Banks and other taxpayers which are required to submit periodical financial reports should base their installments on such reports, as adjusted for fiscal purposes.

Monthly installments must be paid by the 15th of the following month and the corresponding monthly return must be filed by the 20th of that month.

Returns

Companies are required to self-assess and lodge annual corporate income tax returns. Consolidated returns for commonly owned entities are not permitted. The returns must be lodged with the relevant Tax Office within four months after the end of the calendar year or tax year and this deadline may be extended for two months by notifying the DGT.

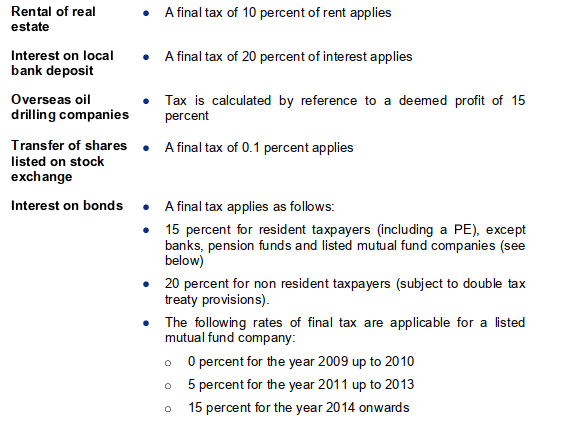

Special rules

Certain types of activities are subject to tax based on special rules, including:

Leasing companies

In 1991, a decree was issued by the MOF that effectively treated leasing companies as financial institutions for tax purposes. The decree requires the adoption of the finance lease accounting method for all qualifying leases. A doubtful debts provision equal to 2.5 percent of the average opening and closing receivables balance is allowed as a tax deduction. This allowance for tax purposes was re-stated in a regulation issued in April 2009.

This 1991 decree (which is still valid) also detailed guidelines on what lease transactions can be undertaken by a leasing company and how leases will be classified between operating and finance leases. Payments of lease installments under a lease classified as a finance lease to an Indonesian leasing company are exempt from VAT. The interest element is subject to withholding tax. Payments made on leases that qualify as operating leases are subject to both withholding tax and VAT.