Double Tax Relief

Indonesia grants a credit for withholding taxes directly paid on income received or accrued in a foreign country. There is no credit for taxes on underlying profits. The credit is only granted if the income is taxable in Indonesia as being part of worldwide earned income. The credit is limited to the lesser of the tax payable in Indonesia on the foreign income or the amount of the foreign tax paid

If the foreign tax is reduced or refunded, the credit will be reduced and the tax payable in Indonesia will have to be increased by the amount of the reduction or refund in the year that such a refund or reduction is made.

Withholding Taxes

Transactions with Non-residents

Withholding tax is imposed at 20 percent on various amounts payable to non-residents, unless the non-resident has a PE in Indonesia, whereby the rates applicable to payments to residents apply. The withholding tax may be reduced where the foreign resident is exempt or eligible for a reduced withholding tax rate by virtue of a DTA.

In order to qualify for any relief under a relevant tax treaty, non residents must provide a certificate from the tax authority in their country of residence (Form DGT1 for most taxpayers).

In addition to providing details of tax residence status, non-bank foreign entities must make a declaration regarding other details of their businesses on Form DGT1, such as:

- the entity/transaction structure is not motivated by tax avoidance;

- the entity is independently managed;

- the entity employs sufficient qualified personnel;

- the entity has business activities;

- the company is subject to tax in its jurisdiction on the Indonesian-sourced income; and

- 50 percent or more of total income is not used to fulfill obligations to other parties in the form of interest, royalty or other remuneration.

Further clarification has been issued on what is meant regarding some of the above declaration requirements.

Banks, pension funds and certain others using custodian banks may use an alternative form (Form DGT2) which requires only certification of the tax residency status, without the above additional declarations regarding the business or transaction.

Withholding tax applies to the following:

- Dividends

- Interest, including premiums, discounts and compensation for loan guarantees

- Royalties

- Rent and other income connected with use of property

- Cross border leases

- Gifts and awards

- Compensation for work by individuals or services or activities by overseas entities (applies whether services are performed outside or inside Indonesia)

- Insurance premiums (the rate of tax is reduced depending on the nature of the transaction)

-Insured – 10 percent

-Insurance company – two percent

-Reinsurance company – one percent. - Disposals of shares in unlisted Indonesian companies. The effective rate of tax is 5 percent. Where a foreigner is buying the shares in a company, the company must pay the tax before the transfer of ownership is recorded.

Branch Profits Tax

PE’s of foreign enterprises are subject to 20 percent withholding tax on their after-tax income unless eligible for a reduced rate by virtue of a DTA.

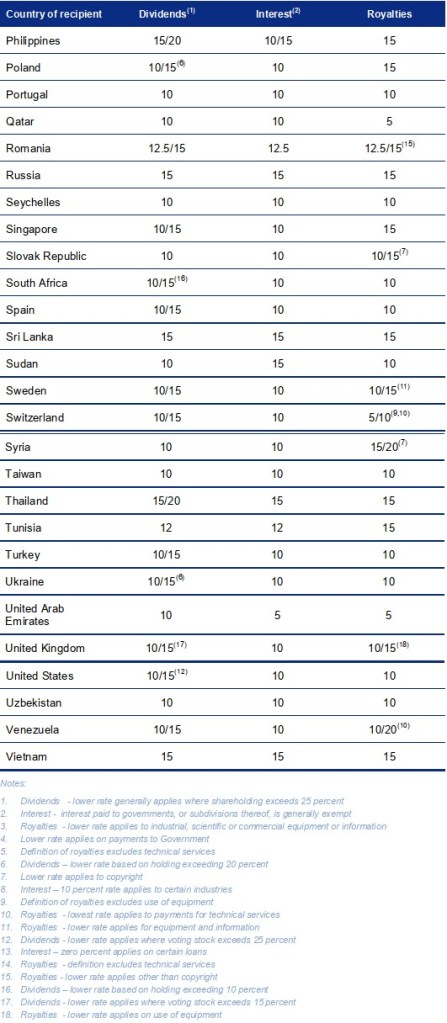

Double Tax Agreements

As of 31 December 2011, Indonesia has signed DTA’s with 59 countries. The following withholding tax rates apply to recipient countries that do not have a PE or fixed base in Indonesia.

In addition treaties with the following countries have been signed but are not yet in force:

Armenia

Hong Kong

Myanmar

Papua New Guinea

Philippines (amended)

Surinam

Tajikistan