A corporation, for tax purposes, is classified as “resident” or “nonresident”. Residency is determined on the basis of place of incorporation. A corporation is therefore considered “resident” if incorporated in Indonesia and non-resident if incorporated elsewhere.

Resident corporations are taxed on their worldwide income. Tax credits are allowed for income that has been taxed outside the country. Non-residents are taxed only on income derived from Indonesian sources, subject to any relief available under double taxation agreements. However, a non-resident entity with a permanent establishment (PE) in Indonesia, such as a branch office, is taxed on:

- the PE’s income from its business or activities, and from the assets it owns and controls;

- the income of the head office arising from business activities, or sales of goods or services in Indonesia of the same type as those sold by the permanent establishment in Indonesia; and

- all other income, either received or accrued by the head office such as dividends, interest, royalties, rent and other income connected with the use of property, fees for services, etc, provided that the property or activities producing the income is effectively connected with the PE in Indonesia.

Income attributable to a PE of a company that is resident of a treaty country should be referred to the relevant treaty.

In Indonesia, a PE is generally defined as an operation in which a non-resident establishes a fixed place of business in Indonesia. This would include a management location, a branch office, an office building etc. A PE can also be established as a result of the nonresident entity’s employees providing services in Indonesia for more than 60 days in any 12-month period. For companies from those countries with which Indonesia has concluded a Double Tax Agreement (DTA), the relevant definition may be somewhat modified.

Taxable income

Taxable income is defined as any increase in economic prosperity received or accrued by a taxpayer, whether originating from within or outside Indonesia that may be used for consumption or to increase the recipient’s wealth in whatever name and form. It includes any remuneration in connection with work or services, business profits (with no distinction between operating and capital income), dividends, interest, rent, royalties and other income related to the use of property. Certain income is exempt from tax, such as dividends earned by a domestic corporation from another domestic corporation, provided that the dividend is from the retained earnings and the shareholding of the recipient is at least 25%.

Calculation of Taxable Income

Taxable income is calculated after the deduction of allowable Deductible Expenses (DE). For individuals there are income tax exclusions (PTKP), but set at relatively low income levels. Individuals are broadly liable to income tax on cash income. Benefits-in-Kind (BIK) provided by employers to employees are not taxable to individuals, but are a non-deductible expense (NDE) against corporate taxable income. For a representative office however, which is not considered as a corporate taxpayer, the BIK provided to their employee is taxable to the employee. Employers are required to withhold income tax from employees and deposit it each month with the State Treasury (Kas Negara). Employers prepare a consolidated annual tax return detailing each employee’s individual tax calculation. The employee should then file a separate personal return. Normally, tax returns should be filed by 31 March of the year following the calendar year; corporate tax returns however, can be filed four (4) months after the closing of the book year.

Corporate taxable income is calculated after deduction of most normal business expenses. Rates of depreciation are regulated though taxpayers may elect either the straight line or double declining method. Provisions are not deductible nor are employee benefits-inkind as mentioned above. Companies may choose to be taxed on the basis of a financial year other than the calendar year. Books of account may be kept in the English language based on the approval from the Director General of Taxation. Foreign currency, e.g. U.S. dollars may also be used as the reporting currency if appropriate approval is obtained. Annual filings should be lodged within 4 months of the end of the financial year. In certain cases however, the company can apply for an extension.

Exemption from income for capital increase

Taxable income is determined by subtracting allowable deductions from revenue. Certain expenses, such as employee benefits-in-kind and donations, are generally not tax deductible. In addition, interest incurred to finance the acquisition of shares is not deductible unless dividends from the shares purchased are taxable. The following are major allowable deductible expenses:

1. Business Expenses

As a general rule, taxpayers may deduct from gross income all expenses related to earning, securing and collecting taxable income. Items that are not deductible include those incurred for the personal benefit of shareholders; benefits-in-kind (e.g. housing and vehicles) provided to employees, except for the provision of food and beverages for all employees and for certain benefits-in-kind provided to employees in certain remote areas; gifts; donations and support; “excessive” payments for goods or services where a special relationship is deemed to exist between the buyer and seller; and expenses incurred in the course of producing income that is exempt from tax or subject to final tax. Formation of a reserve or allowance is generally not tax deductible, with the exception of bad debt allowances for banks or finance leasing companies, reserves in insurance companies, and reserves for reclamation costs in the mining industry.

2. Research and Development

Expenses such as those for research and development carried out in Indonesia and eligible employee training qualify as regular allowable deductions. Indonesia has no special income tax deductions/relief for research and development and eligible employee training. The deductibility of research and development performed offshore remains unclear.

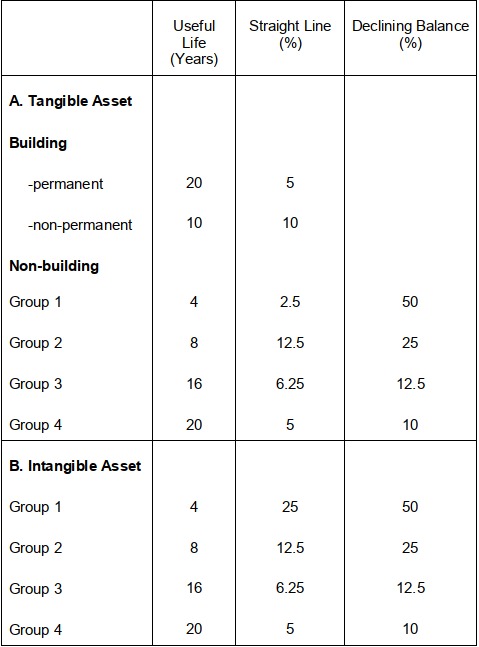

3. Depreciation and Amortization

Investors can adopt either the straight line or the double declining balance method for depreciation of tangible assets (except buildings). The taxpayer should apply the depreciation method chosen consistently. The Tax Office must approve any change in method. The same depreciation method and percentages are allowed for intangible assets with a benefit of more than one year.

The table below shows the allowable useful life of the assets as categorized and the annual depreciation rates:

Tax base

The tax base on a corporate is any income from:

- the business or activities, and from the asset owned or controlled,

- any income of the head office from the business or activities, sales of goods, or services rendered in Indonesia, and

- Any income received or accrued by the head office, as long as there is an effective relationship between the permanent establishment and the assets or activities that provide such income.

The costs related to the income may be deducted from the income of the corporate.

Tax rates

The corporate tax rate starting 2009 is 28%. This rate will be further reduced to 25% at the start of 2010. Micro, small and medium business (MSMEs / UMKM) may have a tax discount of 50% of the normal rate for turnover of up to Rp 4.8 billion. Companies with a turnover of less than Rp 50 billion a year are categorized as MSMEs / UMKM. Companies that list at least 40% of their shares on the Indonesian Stock Exchange will have a tax cut of 5% from the top rate. This will give them an effective tax rate of 23% in 2009 and 20% in 2010.

Tax credit

At the end of the year, from the tax liability shall be deducted the tax credits for the relevant fiscal year, in the form of:

- Withholding tax on income from any work.

- Tax collection on income from any activity in the import sector or any other business.

- Withholding tax in the form of dividend, interest, royalty, rent, prize, and award, and compensation for service.

- Tax paid or due on income from abroad that may be credited.

- Payment made by the taxpayer.

Inter-company pricing

Article 18 of the Income Tax Law and Article 2 of the Value Added Tax Law provide rules relating to transfer pricing that can be summarized as follows:

- The Director General of Taxation is authorized to re -stipulate amounts of income and deductions for taxpayers who have special relationships

- The Director General of Taxation is authorized to make agreements with taxpayers and cooperate with tax authorities of other countries to determine transaction prices between parties having special relationships

Indonesia adopts a self-assessment system, however the taxpayers is required to include any transfer price information in their tax returns. Starting 2007 Government Regulation put in place a mandatory requirement to maintain and keep the formal documentation for transfer price. For fiscal year 2009, the tax payers should use new form for corporate income tax return which requires a lot of information for transfer price. The tax payers are also require preparing the transfer pricing documentation and file it together with the tax return. Therefore, the tax authorities can obtain the transfer price information from the tax return. Furthermore, under the self-assessment system, tax audit is a very important task for the authorities to ensure compliance by taxpayers and thus there are always realistic risks that explanations/details of related party transactions will be demanded during tax audits.

Eventhough in Indonesia, there is currently no separate tax audit or audit teams to review only transfer pricing, however in practice the tax authorities put significant increase in focus on transfer pricing issue in tax audits, with large tax corrections related to transfer pricing issues proposed in many cases. Transfer pricing is rather included as one of the review items in the general tax audit (covering overall corporate and value added tax etc). Examples of transfer pricing issues that have commonly arisen in past general tax audits include:

- Processing fee of toll manufacturer / selling price of contract manufacturer

- Third party domestic selling price vs. related party export price

- Various service fees (e.g. management fee, technical assistance fee to parent company)

- Royalty

- Free / low interest parent loan

Processing fee in (a) and various payments of (c) and (d) are also subject to value added tax and therefore, these types of transfer prices may be scrutinized by the tax authorities not only for corporate tax purposes but also for value added tax purposes. In addition to the transfer price risk, because activities of toll manufacturing subsidiaries were deemed to have created permanent establishments (PE) of parent companies in recent tax audit cases, a PE risk needs to be considered as well in adopting a toll manufacturing structure. Therefore, in order to minimize the PE risk, it may be advisable to consider a contract manufacturing structure rather than a toll one, although the transfer price risk still exists with either structure.

Returns and payment

If the tax liability in a fiscal year appears to be less than the amount of tax credit, after audit, the tax overpayment shall be refunded after being calculated with the other tax liabilities and their sanctions.

If the tax liability in a fiscal year appears to be larger than the tax credit, the underpayment of tax liability must be paid before the Annual Tax return is submitted, for which the deadline is four (4) months after the closing of the book year.