Foreign loan-funded and foreign grant-funded government projects

Government projects funded with foreign loans or foreign grants may be eligible for special tax treatment for the income derived from that funding. The projects that typically qualify are set out in the state Project Table of Contents (Daftar Isian Proyek/DIP) or other similar documents.

Main contractors, consultants and suppliers for foreign grant-funded or loan-funded government projects may have their income tax liability borne by the government. This facility is not available for second-level contractors, consultants and suppliers.

Apart from the above concessions, the main contractors, consultants and suppliers also enjoy the following tax facilities on the importation of goods and the use of foreign taxable services and/or foreign intangible goods for foreign grant-funded or foreign loan-funded government projects:

• Exemption from import duty;

• Non-collection of VAT and LST;

• Non-collection of Article 22 Income Tax on imports.

If a qualifying project is only partially funded by a foreign loan or a foreign grant, the tax facilities are determined proportionally to the amount of the foreign loan or foreign grant.

Public Private Partnership/PPP (Kerjasama Pemerintah dengan Badan Usaha)

This facility is intended to promote and improve cooperation between the government and business entities with respect to the provision of infrastructure and social services. The facility can be approved by the MoF based on the proposal from the responsible institution for cooperation projects.

Integrated Economic Development Zones

Companies conducting business in an Integrated Economic Development Zone (Kawasan Pengembangan Ekonomi Terpadu/KAPET) may enjoy tax facilities. The designation

of an area as a KAPET is set out in a specific presidential decree.

An Entrepreneur in Bonded Zone/Pengusaha Di Kawasan Berikat (PDKB) in a KAPET may be granted tax facilities in the form of:

• Income tax facilities similar to Inbound Investment Incentives under the Income Tax Concessions;

• Non-collection of VAT and LST on importation of certain goods;

• Exemption of Article 22 Income Tax on importation of certain goods;

• Postponement of import duty on capital goods and equipment, and goods and material for processing;

• Non-collection of VAT and LST on the domestic purchases of certain goods.

Bonded Stockpiling Area

Bonded Stockpiling Area (Tempat Penimbunan Berikat) currently consists of:

1. Bonded Zone;

2. Bonded Warehouse;

3. Bonded Exhibition Place;

4. Duty Free Shop;

5. Bonded Auction Place;

6. Bonded Recycling Area; and

7. Bonded Logistic Centre.

We will only highlight three prominent areas in the below sections.

The tax facilities in these areas are as follows:

• Non-collection of VAT and LST on importation of certain goods;

• Non-collection of Article 22 Income Tax on importation of certain goods;

• Postponement of import duty on certain goods;

• Exemption of excise on importation of certain goods; and

• Non-collection of VAT and LST on the domestic purchases of certain goods.

Bonded Zones

The Bonded Zone (Kawasan Berikat) facility is provided to manufacturing companies with export orientation, import substitution, supporting downstream industry, and certain industries such as aircraft, shipbuilding, railways, and the defense & security industry. There is a domestic sales quota of 50% of the previous year export realisation value and/

or sales value to other Bonded Zones/Free Trade Zones/ Special Economic Zones/other places within Customs Area.

Bonded Warehouse

The Bonded Warehouse (Gudang Berikat) facility is intended to store imported goods which can be processed with one or more simple activities within one year.

Bonded Logistic Centre

The Bonded Logistic Centre (Pusat Logistik Berikat) facility is similar to the Bonded Warehouse facility, however, it is intended to store both imported goods from outside the Customs Area and/or goods from other places within the Indonesia Customs Area which can be processed with one or more simple activities within three years.

Free Trade Zones

Goods entered into and goods delivered amongst companies inside Free Trade Zone (FTZ) or Kawasan Perdagangan Bebas may also enjoy tax facility.

Taxpayers in FTZ are entitled to the following tax facilities:

•Exemption of VAT and LST on importation of certain goods;

•Non-collection of Article 22 Income Tax on importation of certain goods;

•Exemption of import duty on certain goods;

•Exemption of excise on importation of certain goods;

•Non-collection of VAT and LST on the domestic purchases of certain goods; and

•Transactions of intangible goods and taxable services are exempted from VAT, except for those delivered to other Indonesia Customs area and Bonded Stockpiling Area or Special Economic Zones companies.

Special Economic Zones

Taxpayers conducting business in Special Economic Zones (Kawasan Ekonomi Khusus/KEK) may enjoy tax facilities. The business should cover the main activities determined for each KEK. The designation of an area as a KEK is set out in a specific government regulation.

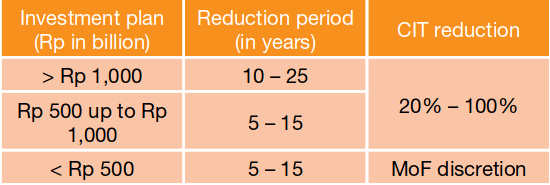

CIT Reduction facility may be granted for new taxpayers with new capital invested in the production chain of main activities in KEK, as described below:

Taxpayers being rejected for the CIT Reduction facility and taxpayers carrying out other activities in KEK, may apply for similar Tax Allowance under the Income Tax Concessions (please refer to pages 68-69 on the relevant tax concession).

On top of the above income tax facilities, taxpayers in KEK are also entitled to the following tax facilities:

• Non-collection of VAT and LST on importation of certain goods;

• Non-collection of Article 22 Income Tax on importation of certain goods;

• Postponement of import duty on capital goods and equipment, and goods and material for processing;

• Exemption of excise on importation of goods to be used to produce non-excisable goods; and

• Non-collection of VAT and LST on the domestic purchases of certain goods.

Industrial Zone

The determination and licensing of an Industrial Zone (Kawasan Industri/KI) are as granted by the government. The applicable tax facilities depend on the classification of the Industrial Development Area/IDA (Wilayah Pengembangan Industri/WPI) of the KI, namely:

1.Advance IDA (WPI Maju/ WPIM)

2.Developing IDA (WPI Berkembang/ WPIB)

3.Potential I IDA (WPI Potensial I/ WPIP I)

4.Potential II IDA (WPI Potensial II/ WPIP II)

Below are the available tax facilities for each type of WPI:

** The applicable period of import duty exemption varies depending on the KI classification and the business cycle of the respective taxpayer, e.g. construction or developing stage.

BKPM Masterlist facility

BKPM may also provide import duty exemption through the issuance of a Masterlist facility for importing machinery and raw materials. An importer can also obtain an exemption from VAT, LST, and/or Article 22 Income Tax by applying to the DGT for approval.

Tax Exemption and Drawback Facilities for Exports

Tax facilities under the scheme of ease of imports for the production of goods to be fully exported (Kemudahan Impor Tujuan Ekspor/KITE) are as follows:

KITE Exemption

This exemption facility allows for most raw materials and sample goods to be imported without payment of import duty, provided that the finished products are exported. The VAT and/or LST on such importations are not-collected either.

Further incentives are also available for small to medium enterprises, whereby the operational requirements are less stringent. The import duty, VAT and/or LST exemptions are available on the importation of raw materials, sample goods, and machinery.

KITE Drawback

This drawback facility allows for the recovery of import duty paid on imported raw materials that are incorporated into finished products which are subsequently exported.