General

Indonesian income tax is collected mainly through a system of withholding taxes. Where a particular item of income

is subject to withholding tax, the payer is generally held responsible for withholding or collection of the tax. These withholding taxes are commonly referred to using the relevant article of the Income Tax (Pajak Penghasilan/PPh) Law, as follows:

(i)Article 21 income tax (PPh 21)

Employers are required to withhold PPh 21 from

the salaries payable to their employees and pay the tax to the State Treasury on their behalf. The same withholding tax is applicable to other payments to non-employee individuals (e.g., fees payable to individual consultants or service providers) (see page 18 for

the relevant tax rates). Resident individual taxpayers without an NPWP are subject to a surcharge of 20% in addition to the standard withholding tax.

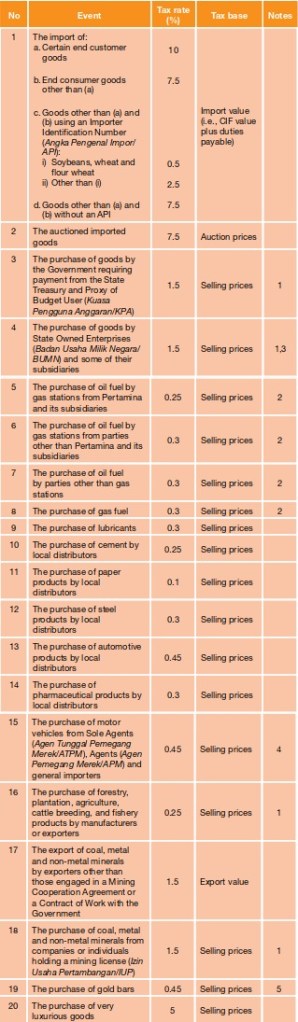

(ii)Article 22 income tax (PPh 22)

PPh 22 is typically applicable to the payments of the following events:

Notes:

1. In events (3), (4), (16), and (18), the PPh 22 collectors must withhold PPh 22 from the amount payable to a particular vendor, except payments for the purchase/use of:

a)oil fuel, gas fuel, lubricants, postal products;

b)water and electricity;

c)oil, gas (including upstream by products) from a Contractor of a PSC, the Contractor’s head office, or the Contractor’s trading arms; and

d)geothermal or electricity from a Contractor of a Joint Operation Contract.

There is also an exemption for the purchase of goods with a value of up to Rp 2 million, Rp 10 million, and Rp 20 million for events (3), (4), and (16) respectively. In the other events, the importer or the buyer of the designated goods must pay PPh 22 in addition to the amounts payable for the goods imported or purchased.

2. The withheld PPh 22 constitutes a pre-payment of corporate/individual income tax liabilities, except for the purchase of oil and gas fuel by distributors/agents, which is categorised as final tax.

3. Exception applies on the purchase of forestry, plantation, agriculture, cattle breeding, and fishery products since it is already subject to PPh 22 in event (16).

4. Exception applies on the purchase of very luxurious motor vehicles since it is already subject to PPh 22 in event (20).

5. Exemption applies on the sale to Bank Indonesia.

6. The tax does not apply, either automatically or with an Exemption Certificate issued by the DGT, on the following types of events:

a)Import/purchase of goods not subject to income tax.

b)Import of goods exempted from import duties and/or Value Added Tax (VAT), including if the goods is subject to 0% import duty, or VAT is not collected.

c)Goods that have been temporarily imported (i.e. goods for re-export).

d)Goods for re-importing (i.e., exported and re-imported in the same quality or to be repaired/tested).

e)Import of gold bars for the production of jewellery for re-export.

f)Purchase of goods related to the use of the government school operations subsidy (Bantuan Operasional Sekolah/BOS) fund.

g)The purchase of grain or rice by the State Treasury, KPA, and the Bureau of Logistics (Badan Urusan Logistik/BULOG).

h)The purchase of basic necessity foods by BULOG or appointed BUMNs.

Taxpayers without an NPWP will be subject to a surcharge of 100% in addition to the standard tax rate.

(iii)Article 4 (2) – final income tax (PPh Final)

Resident companies, PEs, representatives of foreign companies, organisations and appointed individuals are required to withhold final tax from the following gross payments to resident taxpayers and PEs:

Notes:

1.This includes land owner’s income from Build Operate Transfer agreements.

2.Proceed from the transfer of real estate assets to a Real Estate Investment Fund (Kontrak Investasi Kolektif – Dana Investasi Real Estate/ KIK-DIRE) is subject to 0.5% tax rate.

3.Different rates apply on interest received from time deposits sourced from export proceeds (Devisa Hasil Ekspor).

4.If the recipient is a mutual fund registered with the Financial Services Authority (Otoritas Jasa Keuangan/OJK), the tax rate is 5% until 2020 and 10% thereafter. If the recipient is a non-resident taxpayer, the tax rate is 20% or a lower rate in accordance with the relevant tax treaty.

5.This regime is optional for eligible taxpayers and only applicable for certain period of time depending on the type of taxpayer.

(iv)Article 23 income tax (PPh 23)

Certain types of income paid or payable to resident taxpayers are subject to PPh 23 at a rate of either 15% or 2% of the gross amounts:

a. PPh 23 is due at a rate of 15% of the gross amounts on the following:

1. Dividends (but see pages 12-13 concerning profit distributions);

2. Interest, including premiums, discounts and loan guarantee fees;

3. Royalties;

4. Prizes and awards.

b. PPh 23 is due at a rate of 2% of the gross amounts on the fees for the following:

1. Rentals of assets other than land and buildings;

2. Compensation with respect to technical services, management services, consultation services and other services, except those have been withheld of Income Tax as referred to Article 21.

(v)Article 26 income tax (PPh 26)

Resident taxpayers, organisations and representatives of foreign companies are required to withhold tax at a rate of 20% from the following payments to nonresidents:

a.On gross amounts:

1. Dividends;

2. Interest, including premiums, discounts and guarantee fees;

3. Royalties, rents and payments for the use of assets;

4. Fees for services, work, and activities;

5. Prizes and awards;

6. Pensions and any other periodic payments;

7. Swap premiums and other hedging transactions;

8. Gains from debt write-offs;

9. After-tax profits of a branch or PE.

b. On Estimated Net Income (ENI), being a specified percentage of the gross amount:

Where the recipient is resident in a country which has a

tax treaty with Indonesia, the withholding tax rates may be reduced or exempted.